The Homeowners Hard Market Starting to Cool

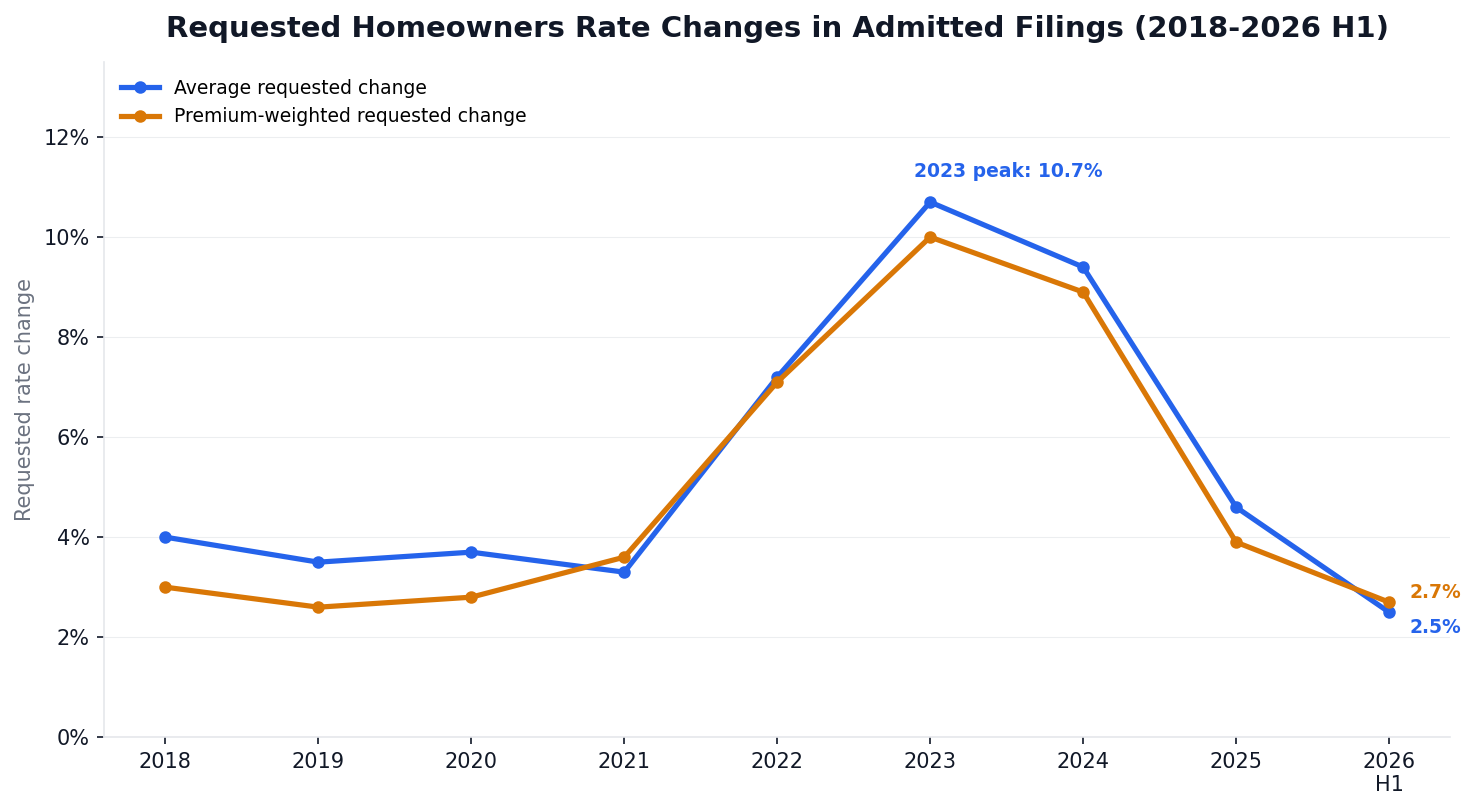

The homeowners market is showing signs of softening for the first time since early 2021. Across more than 40,000 admitted homeowners rate filings submitted to state insurance departments from 2018 to H1 2026, the average requested rate change peaked at 10.7% in 2023. In the first half of 2026 it is 2.5%.

The average line counts every filing equally, from single-county mutuals to national carriers. The premium-weighted line counts each filing in proportion to the premium it covers, so the largest programs matter most. Both peaked in 2023 and both now sit below 3%. Filed changes take effect months after submission, on average about three months for new business and four for renewals, so the filings show a turn before renewal notices do.

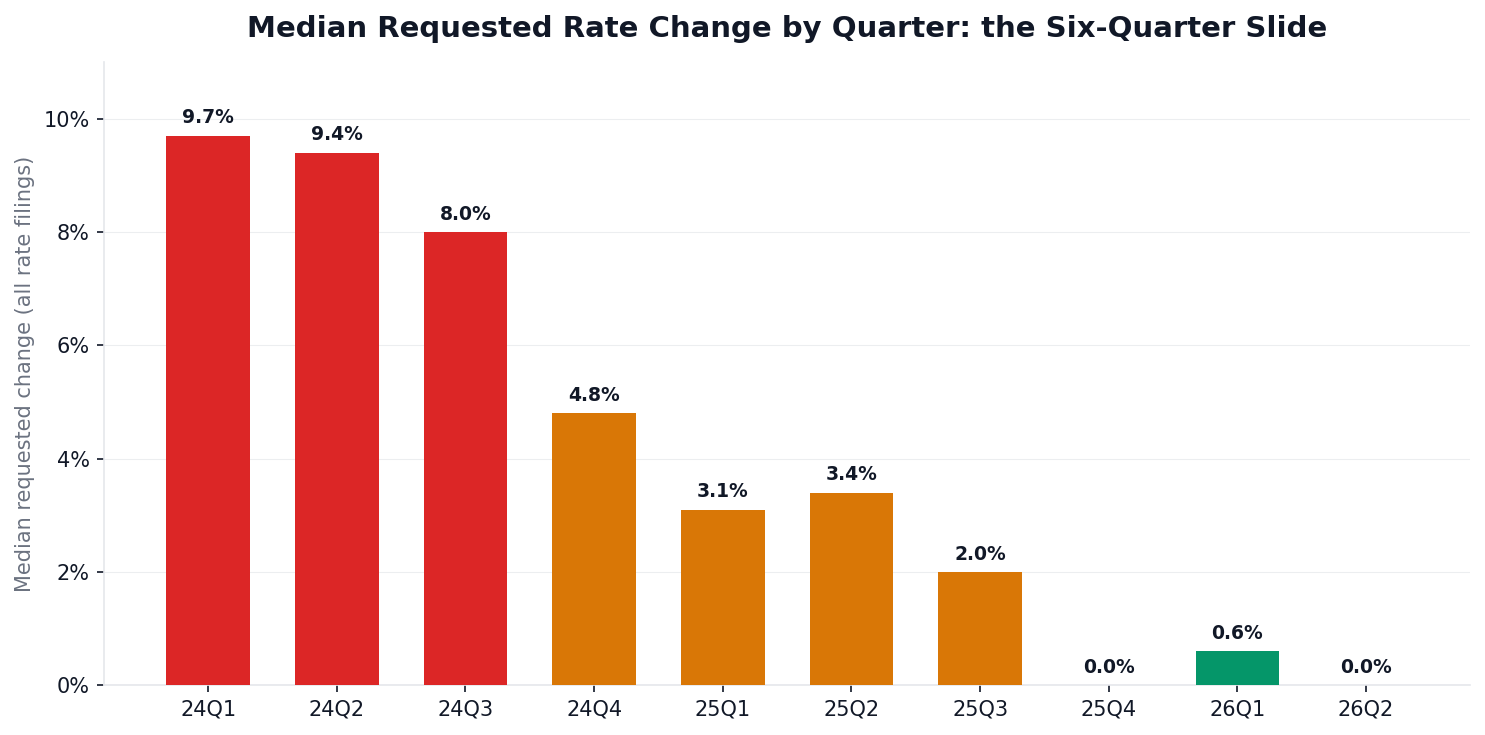

Six quarters from peak to zero

As late as the second quarter of 2024, the median homeowners rate filing asked for 9.4%. Six quarters later, in Q4 2025, the median filing requested nothing at all and has stayed at or near zero through the first half of 2026.

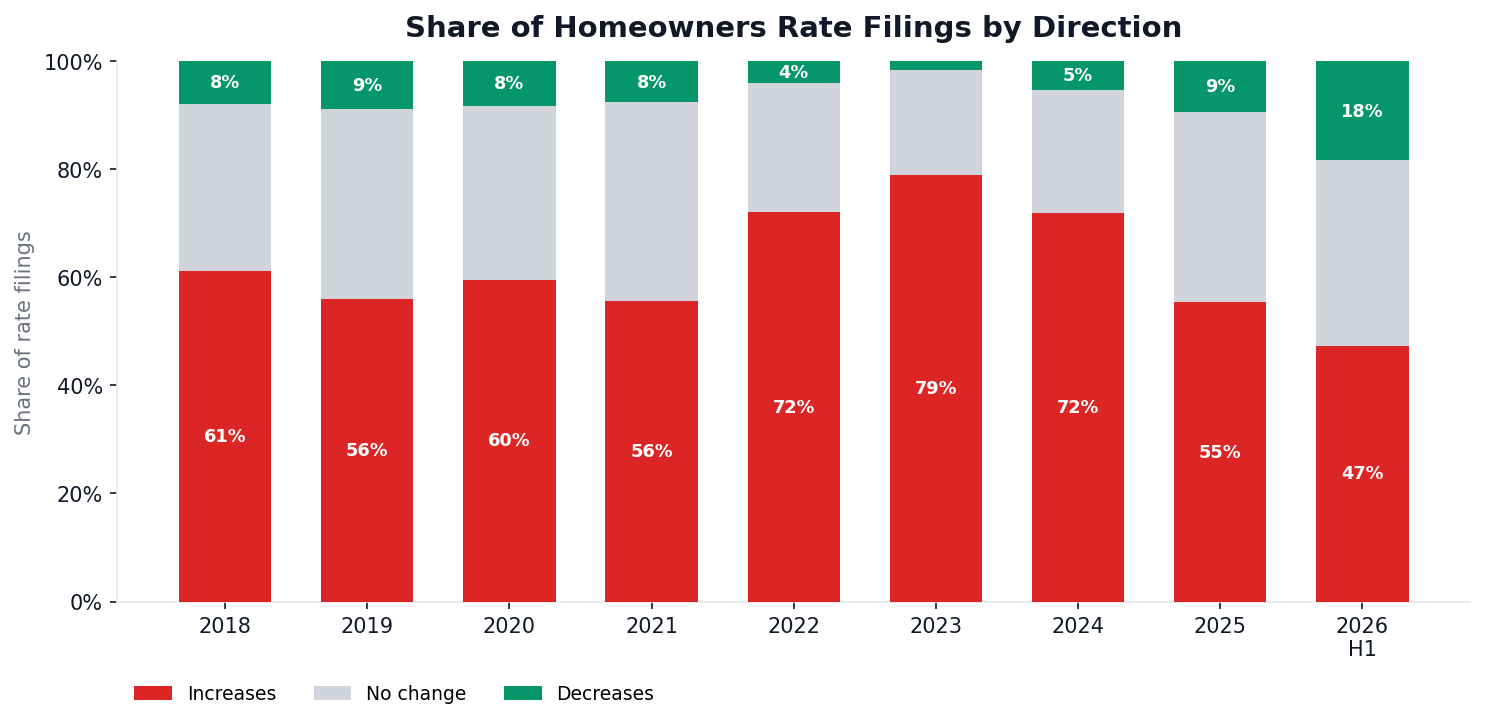

The mix of filings tells the same story from a different angle. In 2023, filings requesting increases outnumbered filings requesting decreases 40 to 1. In the first half of 2026 the ratio is under 3 to 1, and 18% of rate filings now request a decrease, double the share of any year since 2018.

Filing volume itself is falling too, from 5,943 rate filings in 2023 to 4,292 in 2025. Carriers file less often when they are not chasing rate.

Inside the filings: 2023 vs 2026

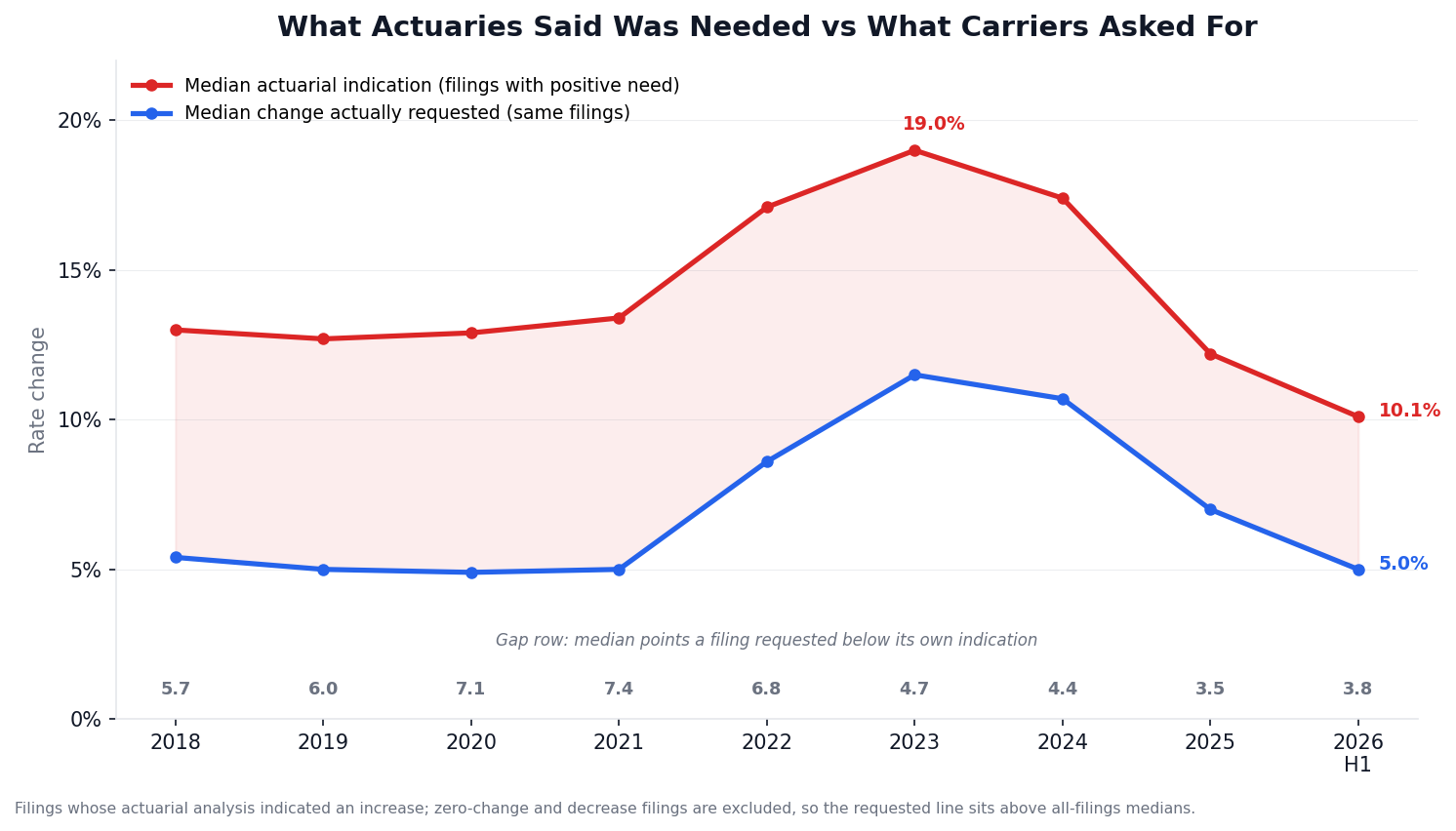

In 2023, carriers needed rate and fought for it. Every rate filing carries an actuarial indication, the change the carrier's own analysis supports. Among filings indicating an increase, the median indication climbed from about 13% before 2022 to 19.0% in 2023, and carriers asked for nearly all of it: in profitable years the median filing requests 6 to 7 points less than its indication to stay competitive, and by 2023 that margin had collapsed to under 5 points.

The back-and-forth matched the stakes. American Family filed for 19.5% in Kansas against a 25% indication and spent five months answering objection letters demanding proof that Kansas hail was worse than its neighbors'. Allstate's 34.1% increase on its $510 million California program took 482 days and multiple objection rounds over its wildfire model switch. Carriers were willing to spend months justifying an ask, and the asks landed: filings withdrawn or rejected never exceeded 5% of homeowners rate filings in any year since 2018.

By 2026 the tone has changed completely. The median indication has fallen to 10.1% as underwriting results recovered, and the typical filing is housekeeping. Allstate filed a 0.8% decrease in Illinois built from segmentation tweaks, stating plainly that "no indication was run for this filing." Travelers filed a 6.4% decrease in Virginia to hit "our selected average rate level change." One of the largest zero-percent filings of the year, covering $1.1 billion of Farmers premium in Texas, is a rules filing complying with a new credit re-scoring law, not a pricing decision.

The rare big ask now gets ground down. Palisades filed for 21.6% in New Jersey in January and drew objections asking, among other things, for "the overall company strategy with writing business in New Jersey." Kemper filed for 16.7% in New York, went quiet under repeated objections, and the state closed the filing with the note that "no policy may be issued utilizing its subject matter."

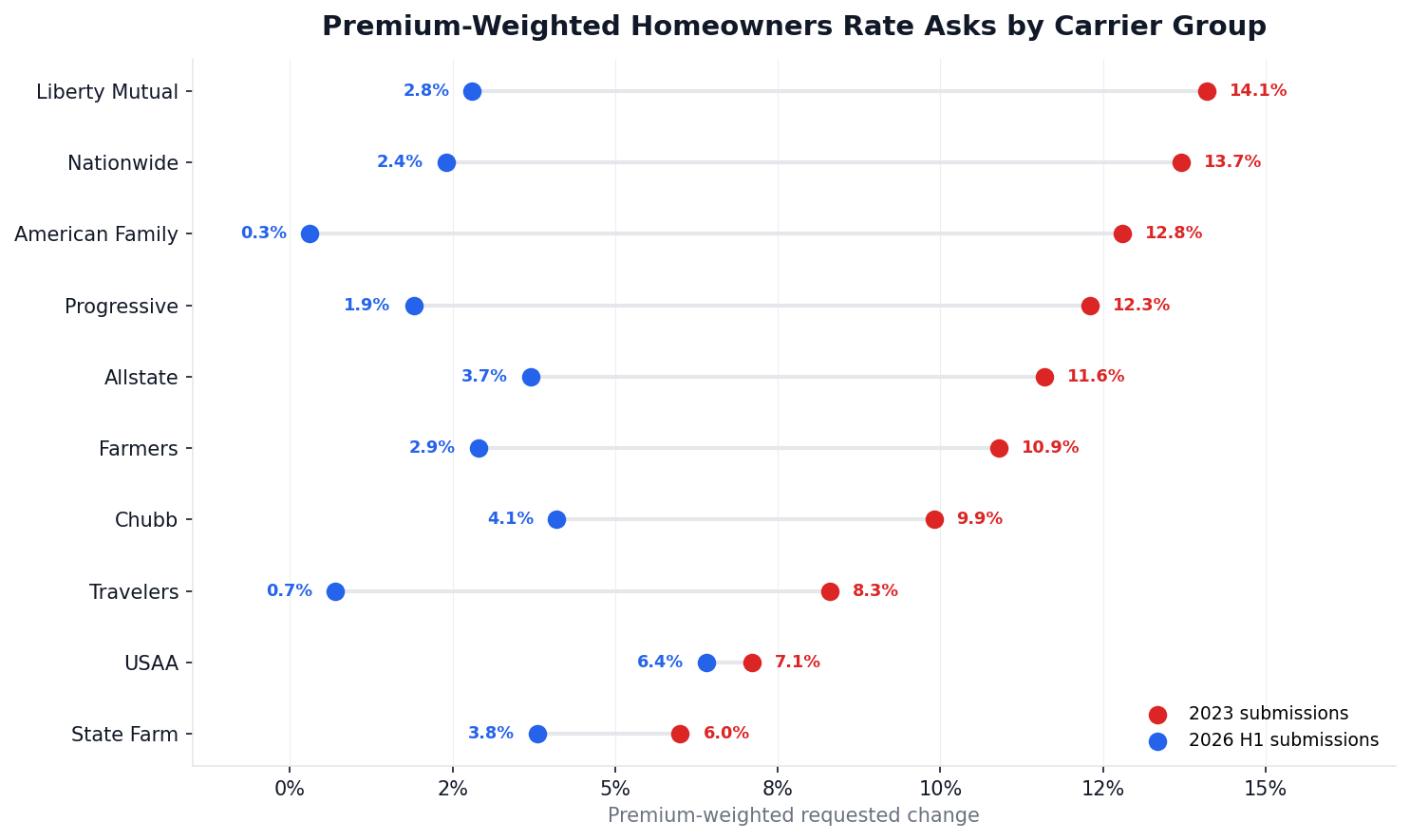

Rate asks by carrier

The same softening runs through the majors, at different speeds.

Liberty Mutual's premium-weighted ask fell from 14.1% to 2.8%. American Family went from 12.8% to 0.3%. Allstate, Nationwide, and Travelers all have 2026 median asks of exactly zero.

Progressive, which files homeowners through its American Strategic companies, ran the cycle late. It kept taking double-digit rate through 2024 and 2025, and its compounded asks since 2022 total 55%, the highest of any major group. In 2026 it too dropped to a 1.9% weighted ask: the last major carrier reaching its target.

USAA is the exception that sharpens the rule. It never spiked, peaking at a 7.1% weighted ask in 2023, roughly half its peers, and it has not gone to zero either: its 2026 ask of 6.4% is its highest since 2023. Steady pricing through the whole cycle.

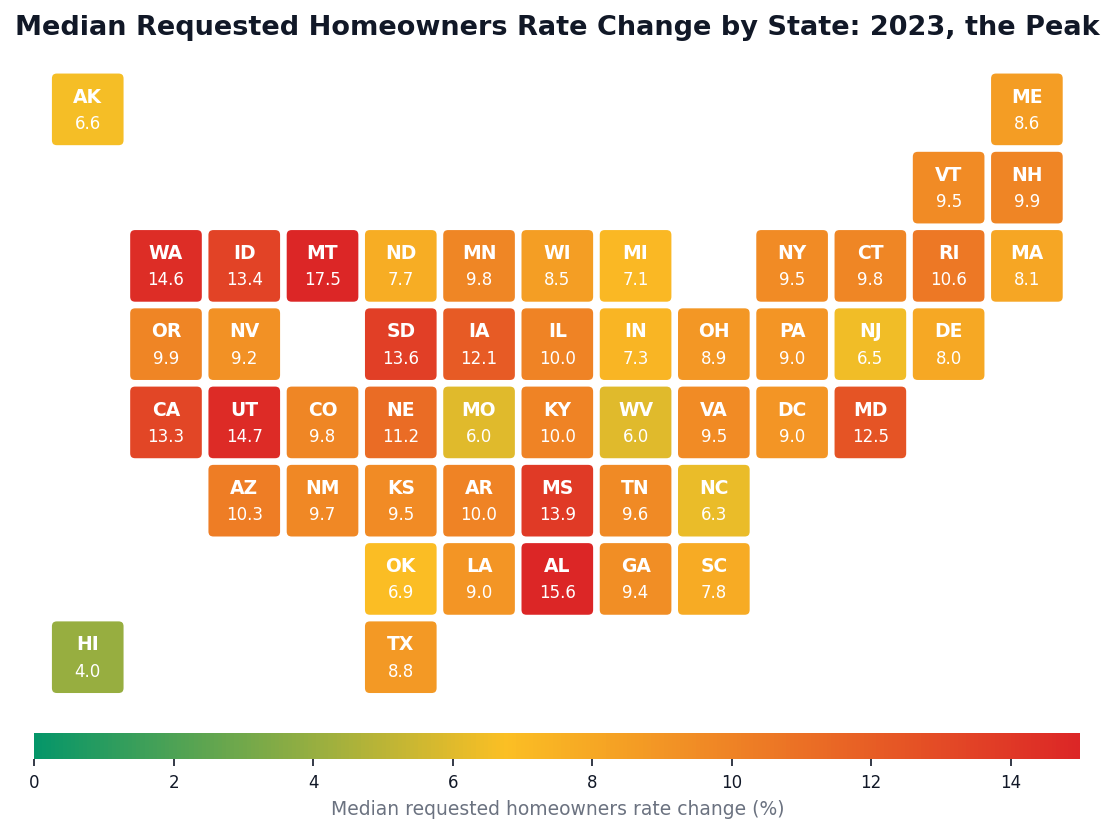

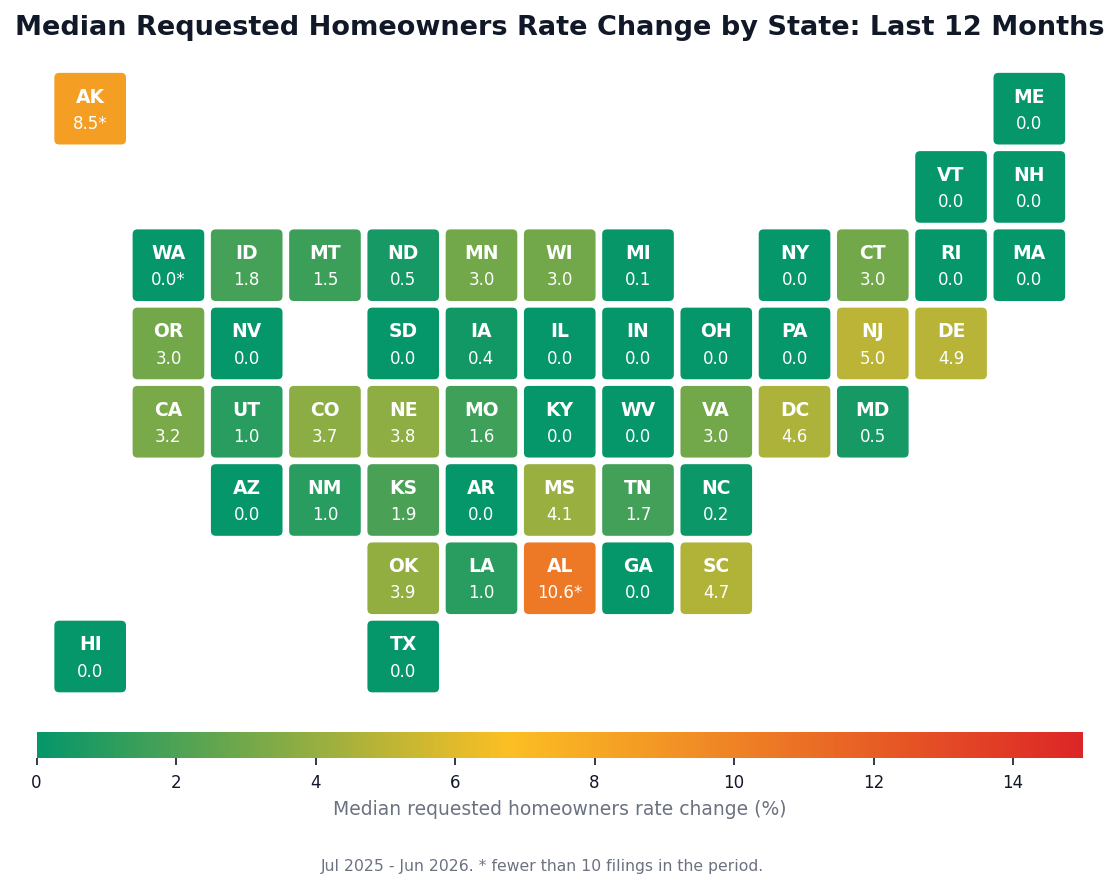

Where it is ending, and where it is not

The state picture is the most dramatic view of the turn. In 2023, nearly every state in the country was orange or red.

Twelve months of filings later, the same map is almost entirely green.

Montana had the highest median ask in the country in 2023 at 17.5%. Over the last 12 months it is 1.5%. Utah went from 14.7% to 1.0%. Texas, with 301 filings in the last year, has a median ask of exactly zero.

New Jersey (5.0%), Delaware (4.9%), South Carolina (4.7%), Mississippi (4.1%), and Nebraska (3.8%) are among the states still running warm.

Where the cycle stands

This is a familiar sequence. Losses rise, rates rise, carriers return to profit, competition returns, rates go flat or fall.

The net direction of filed rates is still slightly up: the premium-weighted ask is +2.7% in the first half of 2026, and just over half of program premium still sits under filings that raise rates. The increases that remain are back to pre-2022 size, a median of 5.0%, the same as 2021. The competitive stage is visible on the other side: 14.6% of program premium now sits under rate-decrease filings, a share last seen in 2019, at the tail of the last soft market.

Data sourced from FilingFocus.

Methodology: Analysis covers admitted homeowners rate filings across all homeowners types of insurance submitted to state insurance departments from 2018 through early July 2026, excluding withdrawn and rejected filings, counted per company program. Rate changes use each filing's reported overall rate impact. Medians cover all rate filings, including those requesting no change; the indication chart covers filings whose analysis indicated an increase. 2026 figures cover January through early July.